R&D is an ever-evolving field. With new technologies and data sources available, what does an R&D researcher do to stay ahead of the curve?

In this blog post, we’ll explore what does an R&D researcher do, the impact of technology on R&D researchers, what it takes to become one, and where the future of R&D is headed.

We’ll also answer that all-important question: What does an R&D researcher do exactly?

Table of Contents

What Does an R&D Researcher Do?

Job Description and Responsibilities

Skills and Qualifications Required for the Role

How to Become an R&D Researcher

The Impact of Technology on R&D Research

Automation and Artificial Intelligence

What is Research in R&D?

Research is a type of scientific inquiry that focuses on the development and improvement of products, processes, services, or technologies. It typically involves experimentation and analysis to find solutions to problems or create new products.

Research can be conducted in-house by a company’s own R&D team or externally through partnerships with universities and other organizations.

The research component of R&D includes both basic and applied science as well as engineering activities such as design, testing, prototyping, and optimization. The goal is to develop better products faster than competitors while staying within budget constraints.

Types of R&D Research

There are several types of R&D research.

- Fundamental (basic) research seeks to understand the underlying principles behind phenomena.

- Exploratory (preliminary) studies explore potential solutions without committing resources.

- Applied (developmental) research focuses on developing specific applications from existing knowledge.

- Commercialization studies involve taking an idea from its concept stage through product launch.

- Evaluation studies assess the performance characteristics and safety requirements for a given product.

- Market surveys/studies measure customer preferences for different features in order to guide product development decisions.

- Cost-benefit analyses compare costs against expected benefits over time.

- Feasibility assessments evaluate whether proposed projects are technically feasible before committing resources.

- Patent searches/analyses identify potentially infringing patents so companies can avoid costly legal disputes down the road.

Benefits of Research

The primary benefit of conducting research is gaining insight into how to improve existing products or develop new ones. This type of work often yields valuable intellectual property rights such as patents that can provide additional protection against competition in certain markets.

Conducting regular R&D helps keep teams up-to-date with emerging trends in their industry, allowing them to stay ahead when it comes to innovation initiatives.

Key Takeaway: R&D research is an organized effort to discover new knowledge about a product, process, service, or technology for the purpose of improving it. This type of work often yields valuable intellectual property rights such as patents that can provide additional protection against competition in certain markets.

What Does an R&D Researcher Do?

Job Description and Responsibilities

A researcher must identify problems, analyze data, design experiments, evaluate results, and report findings. This role requires strong analytical skills as well as the ability to work independently with minimal supervision.

Skills and Qualifications Required for the Role

To be successful in this role, a researcher should have a bachelor’s degree in engineering or a science-related field such as physics or chemistry. They should also possess the following qualifications:

- Excellent problem-solving skills.

- Knowledge of laboratory techniques.

- Familiarity with computer programming languages.

- Experience working with statistical software packages.

- Understanding of product development processes.

- Good communication skills both written and verbal.

- Great attention to detail.

- Creativity when it comes to developing solutions for complex problems.

So what does an R&D researcher do?

A typical day for an R&D researcher may involve the following tasks:

- Designing experiments based on hypotheses generated from previous research studies.

- Collecting data through laboratory testing or simulations using computers.

- Analyzing collected data using various statistical methods such as regression analysis or machine learning algorithms.

- Documenting results in reports that can be shared internally within the organization or externally with customers, partners and vendors.

- Attending meetings where progress updates are discussed amongst other team members.

R&D researchers: We’re the ones who solve complex problems, design experiments, analyze data and report findings. It’s a tough job but someone has to do it! #researchanddevelopment #innovation Click To Tweet

How to Become an R&D Researcher

Becoming an R&D researcher requires a combination of education, training, and experience. To start, you’ll need to have at least a bachelor’s degree in a related field such as engineering or science. Depending on the specific role you’re looking for, some employers may require higher levels of education such as master’s degrees or PhDs.

In addition to educational requirements, many employers will also look for professional certifications and licenses that demonstrate your knowledge and skillset in the field. These can include certifications from organizations like the American Society for Quality (ASQ) or the Institute of Electrical and Electronics Engineers (IEEE).

Finally, having relevant work experience is essential for becoming an R&D researcher. Employers typically prefer candidates who have prior research experience in their industry or similar roles within other companies. This could include internships or part-time jobs while completing a degree program.

Additionally, gaining additional technical skills through courses offered by universities or online platforms can be beneficial when applying for these types of positions.

Are you an R&D researcher? Get the education, training, and experience you need to succeed! Plus, don’t forget certifications and licenses that show off your skillset. #ResearchAndDevelopment #RnD Click To Tweet

The Impact of Technology on R&D Research

Automation and Artificial Intelligence

Automation and artificial intelligence (AI) are having a profound impact on the way research is conducted. AI-powered algorithms can quickly analyze large datasets, identify patterns, and generate insights that would be difficult or impossible for humans to uncover. This has enabled researchers to focus their efforts on more complex tasks such as developing new products or processes instead of spending time manually analyzing data.

AI also enables researchers to make faster decisions based on real-time data analysis, allowing them to respond quickly to changing market conditions.

Data Analysis Tools

Data analysis tools are essential for modern R&D research. These tools allow researchers to quickly process large amounts of data from multiple sources into meaningful information they can use in their work.

Popular tools include:

- Statistical software packages like SPSS and SAS,

- Machine learning libraries like TensorFlow and PyTorch.

- Natural language processing frameworks like spaCy and NLTK.

- Visualization programs like Tableau and Power BI.

- Database management systems such as MySQL and MongoDB.

- Predictive analytics platforms such as IBM Watson Analytics.

- Cloud computing services such as Amazon Web Services (AWS), Google Cloud Platform (GCP), and Microsoft Azure Machine Learning Studio (MLS).

- Hadoop clusters for big data processing applications.

Cloud computing is revolutionizing the way research is conducted by providing access to powerful computing resources at an affordable cost. By leveraging cloud services such as AWS or GCP’s Infrastructure-as-a-Service offerings, researchers can easily scale up their computing power when needed without investing in expensive hardware or dealing with complicated setup procedures.

Additionally, cloud providers offer a variety of specialized services tailored specifically for scientific research which enable teams to collaborate efficiently across geographic boundaries while securely storing all their project assets in one place online.

(Source)

The Future of R&D Research

The field of R&D is constantly evolving and the future looks brighter than ever. Emerging trends in the field are focused on automation, data analysis tools, cloud computing, and artificial intelligence (AI).

Automation is becoming increasingly important for streamlining processes and reducing manual labor.

Data analysis tools are being used to quickly analyze large datasets to identify patterns or correlations that may not be visible with traditional methods.

Cloud computing has revolutionized how researchers store and access their data, allowing them to collaborate more easily across teams and locations.

AI is also playing an increasingly important role in R&D research by providing insights into complex problems that would otherwise be difficult or impossible to solve manually.

Challenges facing the industry include a lack of skilled personnel, limited resources, tight budgets, and rapidly changing technology landscapes. To overcome these challenges it’s essential for organizations to invest in training programs that can help develop employees’ skill sets so they can keep up with advances in technology.

Additionally, organizations must ensure they have adequate resources available such as software licenses or hardware needed for specific tasks.

Finally, budget constraints should be taken into account when planning projects so there aren’t any surprises down the line due to cost overruns or other unexpected expenses.

Despite these challenges, there are still many opportunities for growth within this field. New technologies such as blockchain could provide increased security measures when dealing with sensitive information. Big data analytics could lead to better decision-making.

Virtual reality applications could improve product design capabilities. Three-dimensional printing solutions could reduce costs associated with prototyping products. Machine learning algorithms could automate tedious tasks like image recognition.

Natural language processing techniques could enable faster communication between humans and machines. Robotic advancements would make certain processes easier or more efficient. Augmented reality applications would allow users greater control over their environment through digital overlays on physical objects.

As technology continues advancing at an exponential rate, we will continue to see new opportunities arise within this space.

Conclusion

R&D is a vital part of the innovation process. It requires creativity and problem-solving skills to come up with new solutions that can help businesses succeed. By understanding what does an R&D researcher do, we can see how they contribute to the success of a company or organization.

With technology continuing to evolve at a rapid pace, there are many opportunities for R&D researchers to make their mark in the world. As such, those interested in becoming an R&D researcher should take advantage of this exciting field and see where it takes them!

Are you looking for a way to simplify and expedite the R&D process? Cypris is here to help! Our research platform provides teams with all of their data sources in one centralized place, allowing them to quickly gain insights that can be used to create meaningful solutions.

With our platform, your team will save time while simultaneously improving results – giving you an edge over competitors. Take advantage of this innovative solution today and see what it can do for your R&D team!

What Does an R&D Researcher Do? The Power of Innovation

R&D is an ever-evolving field. With new technologies and data sources available, what does an R&D researcher do to stay ahead of the curve?

In this blog post, we’ll explore what does an R&D researcher do, the impact of technology on R&D researchers, what it takes to become one, and where the future of R&D is headed.

We’ll also answer that all-important question: What does an R&D researcher do exactly?

Table of Contents

What Does an R&D Researcher Do?

Job Description and Responsibilities

Skills and Qualifications Required for the Role

How to Become an R&D Researcher

The Impact of Technology on R&D Research

Automation and Artificial Intelligence

What is Research in R&D?

Research is a type of scientific inquiry that focuses on the development and improvement of products, processes, services, or technologies. It typically involves experimentation and analysis to find solutions to problems or create new products.

Research can be conducted in-house by a company’s own R&D team or externally through partnerships with universities and other organizations.

The research component of R&D includes both basic and applied science as well as engineering activities such as design, testing, prototyping, and optimization. The goal is to develop better products faster than competitors while staying within budget constraints.

Types of R&D Research

There are several types of R&D research.

- Fundamental (basic) research seeks to understand the underlying principles behind phenomena.

- Exploratory (preliminary) studies explore potential solutions without committing resources.

- Applied (developmental) research focuses on developing specific applications from existing knowledge.

- Commercialization studies involve taking an idea from its concept stage through product launch.

- Evaluation studies assess the performance characteristics and safety requirements for a given product.

- Market surveys/studies measure customer preferences for different features in order to guide product development decisions.

- Cost-benefit analyses compare costs against expected benefits over time.

- Feasibility assessments evaluate whether proposed projects are technically feasible before committing resources.

- Patent searches/analyses identify potentially infringing patents so companies can avoid costly legal disputes down the road.

Benefits of Research

The primary benefit of conducting research is gaining insight into how to improve existing products or develop new ones. This type of work often yields valuable intellectual property rights such as patents that can provide additional protection against competition in certain markets.

Conducting regular R&D helps keep teams up-to-date with emerging trends in their industry, allowing them to stay ahead when it comes to innovation initiatives.

Key Takeaway: R&D research is an organized effort to discover new knowledge about a product, process, service, or technology for the purpose of improving it. This type of work often yields valuable intellectual property rights such as patents that can provide additional protection against competition in certain markets.

What Does an R&D Researcher Do?

Job Description and Responsibilities

A researcher must identify problems, analyze data, design experiments, evaluate results, and report findings. This role requires strong analytical skills as well as the ability to work independently with minimal supervision.

Skills and Qualifications Required for the Role

To be successful in this role, a researcher should have a bachelor’s degree in engineering or a science-related field such as physics or chemistry. They should also possess the following qualifications:

- Excellent problem-solving skills.

- Knowledge of laboratory techniques.

- Familiarity with computer programming languages.

- Experience working with statistical software packages.

- Understanding of product development processes.

- Good communication skills both written and verbal.

- Great attention to detail.

- Creativity when it comes to developing solutions for complex problems.

So what does an R&D researcher do?

A typical day for an R&D researcher may involve the following tasks:

- Designing experiments based on hypotheses generated from previous research studies.

- Collecting data through laboratory testing or simulations using computers.

- Analyzing collected data using various statistical methods such as regression analysis or machine learning algorithms.

- Documenting results in reports that can be shared internally within the organization or externally with customers, partners and vendors.

- Attending meetings where progress updates are discussed amongst other team members.

R&D researchers: We’re the ones who solve complex problems, design experiments, analyze data and report findings. It’s a tough job but someone has to do it! #researchanddevelopment #innovation Click To Tweet

How to Become an R&D Researcher

Becoming an R&D researcher requires a combination of education, training, and experience. To start, you’ll need to have at least a bachelor’s degree in a related field such as engineering or science. Depending on the specific role you’re looking for, some employers may require higher levels of education such as master’s degrees or PhDs.

In addition to educational requirements, many employers will also look for professional certifications and licenses that demonstrate your knowledge and skillset in the field. These can include certifications from organizations like the American Society for Quality (ASQ) or the Institute of Electrical and Electronics Engineers (IEEE).

Finally, having relevant work experience is essential for becoming an R&D researcher. Employers typically prefer candidates who have prior research experience in their industry or similar roles within other companies. This could include internships or part-time jobs while completing a degree program.

Additionally, gaining additional technical skills through courses offered by universities or online platforms can be beneficial when applying for these types of positions.

Are you an R&D researcher? Get the education, training, and experience you need to succeed! Plus, don’t forget certifications and licenses that show off your skillset. #ResearchAndDevelopment #RnD Click To Tweet

The Impact of Technology on R&D Research

Automation and Artificial Intelligence

Automation and artificial intelligence (AI) are having a profound impact on the way research is conducted. AI-powered algorithms can quickly analyze large datasets, identify patterns, and generate insights that would be difficult or impossible for humans to uncover. This has enabled researchers to focus their efforts on more complex tasks such as developing new products or processes instead of spending time manually analyzing data.

AI also enables researchers to make faster decisions based on real-time data analysis, allowing them to respond quickly to changing market conditions.

Data Analysis Tools

Data analysis tools are essential for modern R&D research. These tools allow researchers to quickly process large amounts of data from multiple sources into meaningful information they can use in their work.

Popular tools include:

- Statistical software packages like SPSS and SAS,

- Machine learning libraries like TensorFlow and PyTorch.

- Natural language processing frameworks like spaCy and NLTK.

- Visualization programs like Tableau and Power BI.

- Database management systems such as MySQL and MongoDB.

- Predictive analytics platforms such as IBM Watson Analytics.

- Cloud computing services such as Amazon Web Services (AWS), Google Cloud Platform (GCP), and Microsoft Azure Machine Learning Studio (MLS).

- Hadoop clusters for big data processing applications.

Cloud computing is revolutionizing the way research is conducted by providing access to powerful computing resources at an affordable cost. By leveraging cloud services such as AWS or GCP’s Infrastructure-as-a-Service offerings, researchers can easily scale up their computing power when needed without investing in expensive hardware or dealing with complicated setup procedures.

Additionally, cloud providers offer a variety of specialized services tailored specifically for scientific research which enable teams to collaborate efficiently across geographic boundaries while securely storing all their project assets in one place online.

(Source)

The Future of R&D Research

The field of R&D is constantly evolving and the future looks brighter than ever. Emerging trends in the field are focused on automation, data analysis tools, cloud computing, and artificial intelligence (AI).

Automation is becoming increasingly important for streamlining processes and reducing manual labor.

Data analysis tools are being used to quickly analyze large datasets to identify patterns or correlations that may not be visible with traditional methods.

Cloud computing has revolutionized how researchers store and access their data, allowing them to collaborate more easily across teams and locations.

AI is also playing an increasingly important role in R&D research by providing insights into complex problems that would otherwise be difficult or impossible to solve manually.

Challenges facing the industry include a lack of skilled personnel, limited resources, tight budgets, and rapidly changing technology landscapes. To overcome these challenges it’s essential for organizations to invest in training programs that can help develop employees’ skill sets so they can keep up with advances in technology.

Additionally, organizations must ensure they have adequate resources available such as software licenses or hardware needed for specific tasks.

Finally, budget constraints should be taken into account when planning projects so there aren’t any surprises down the line due to cost overruns or other unexpected expenses.

Despite these challenges, there are still many opportunities for growth within this field. New technologies such as blockchain could provide increased security measures when dealing with sensitive information. Big data analytics could lead to better decision-making.

Virtual reality applications could improve product design capabilities. Three-dimensional printing solutions could reduce costs associated with prototyping products. Machine learning algorithms could automate tedious tasks like image recognition.

Natural language processing techniques could enable faster communication between humans and machines. Robotic advancements would make certain processes easier or more efficient. Augmented reality applications would allow users greater control over their environment through digital overlays on physical objects.

As technology continues advancing at an exponential rate, we will continue to see new opportunities arise within this space.

Conclusion

R&D is a vital part of the innovation process. It requires creativity and problem-solving skills to come up with new solutions that can help businesses succeed. By understanding what does an R&D researcher do, we can see how they contribute to the success of a company or organization.

With technology continuing to evolve at a rapid pace, there are many opportunities for R&D researchers to make their mark in the world. As such, those interested in becoming an R&D researcher should take advantage of this exciting field and see where it takes them!

Are you looking for a way to simplify and expedite the R&D process? Cypris is here to help! Our research platform provides teams with all of their data sources in one centralized place, allowing them to quickly gain insights that can be used to create meaningful solutions.

With our platform, your team will save time while simultaneously improving results – giving you an edge over competitors. Take advantage of this innovative solution today and see what it can do for your R&D team!

Keep Reading

Chemical R&D, drug discovery, and advanced materials teams face a search problem that most software fail to solve in one place: the chemistry that matters is spread across patents, scientific papers, and chemical structure databases at once. A single relevant compound may be claimed in a recent patent, described in a preprint or journal article, and registered in a structure database under a different name. Answering a real research question, whether a compound is novel, whether a route is protected, whether a class of molecules is crowded, requires connecting all three sources. Software that searches only patents, or only scientific literature, or only chemical structures leaves the team to run separate searches and reconcile the results by hand.

The core requirement is therefore not a better single-source search but a unified one. Software that searches patents, scientific papers, and chemical structures together has to treat them as one connected corpus rather than three silos: chemical structure and substructure search on one side, semantic search across patents and scientific literature on the other, and an R&D ontology underneath that understands how a compound, its uses, and its surrounding technology relate. That is what turns a structure query into an entry point into the patents and papers where the chemistry actually appears, instead of a lookup against a single isolated database.

This article explains how combined patent, scientific paper, and chemical structure search works, why the tools most teams use cover only part of it, and how an AI R&D intelligence approach unifies the three. It is written for chemical R&D and IP teams evaluating how to search chemistry across patents and literature without stitching tools together manually.

Why patents, papers, and chemical structures live in separate tools

The fragmentation is historical, not deliberate. Patent chemical structure search, scientific literature search, and compound databases grew up as separate resources, each excellent at its own slice. The free landscape shows the pattern clearly. SureChEMBL, maintained by the European Bioinformatics Institute, extracts chemical structures from patent documents and makes them searchable by structure, substructure, or structure combined with keywords, holding roughly 17 million compounds drawn from around 14 million patent documents. WIPO PATENTSCOPE offers a free chemical compound structure search across its international patent collection for registered users. PubChem, from the US National Institutes of Health, supports structure search across both patent and non-patent documents and adds biological activity data. The Lens links patents to the scholarly literature behind them.

Each of these is genuinely useful, and each covers one part of the problem. None unifies chemical structure search, patent search, and scientific-paper search into a single connected workflow. A team relying on them runs a structure search in one tool, a patent search in another, and a literature search in a third, then reconciles the overlaps manually, which is slow and prone to missed connections precisely where chemical naming differs across sources. The gap is not any single tool's coverage; it is the seam between them.

How chemical structure search works, and why it beats name search

Chemical structure search matches molecules by their structure rather than by name, which matters because a single compound is referred to inconsistently across patents and papers, by systematic name, trivial name, trade name, or registry number. A structure or substructure query sidesteps that variance. An exact-structure search finds a specific molecule; a substructure or scaffold search finds every molecule containing a defined core, which is how a team identifies a whole congeneric series rather than one compound at a time. For patent chemistry specifically, structure search is the reliable way to find where a compound is claimed or exemplified, because the same molecule may never be named the same way twice across a body of filings.

Structure search has a known limitation that any serious workflow must account for: when compounds are extracted from patent text and images automatically, the extraction can introduce errors, so a structure hit should be confirmed against the underlying patent before it is relied upon. This is a reason to connect structure search directly to the source patents and papers rather than treat a compound database as a standalone answer, and it is one of the advantages of software that unifies structures with the documents they came from.

Why semantic search and an R&D ontology are the connective layer

Structure search finds the compound; it does not find the surrounding knowledge. A compound identified in a patent is only useful in context: the scientific papers describing its synthesis and properties, the other patents claiming related molecules, the technology area it belongs to. Connecting a structure to that context requires searching patents and scientific literature by meaning, not by exact keyword, because chemical terminology is inconsistent and a keyword search misses relevant documents that describe the same chemistry in different words. Semantic search retrieves by meaning, which is what makes the link from a structure to its literature and patent context reliable.

An R&D ontology is the second half of the connective layer. An ontology encodes how compounds, uses, methods, and technologies relate, so a search returns a connected picture of a chemistry area rather than a flat list of documents that happen to share a term. Together, chemical structure search, semantic search, and an R&D ontology are what let one query span structures, patents, and scientific papers and return a unified result. Without semantic search and an ontology, combining the three sources remains a manual reconciliation task no matter how many databases a team has access to.

From structure search to prior art, FTO, and white space analysis

A combined patent, paper, and chemical structure search is rarely the end goal; it is the input to an IP or strategy decision. Once a structure search identifies where a compound or scaffold appears across patents and literature, the natural next steps are prior art search, freedom-to-operate (FTO) analysis, and white space analysis. Prior art asks whether the chemistry is novel. FTO asks whether commercializing it would infringe active patent claims. White space analysis asks whether a region of chemical and technology space is genuinely open, which for chemistry means checking scientific literature and commercial signals, not patents alone.

When structure search, patent search, and literature search sit in separate tools, each of these downstream steps requires re-exporting and re-searching, and the analysis fractures across platforms. When they sit in one environment, a structure-driven question flows directly into prior art, FTO, and white space analysis on the same connected corpus. That continuity is the practical payoff of unifying patents, papers, and chemical structures: the search and the decision it feeds happen in the same place.

Where Cypris fits

Cypris is an AI R&D intelligence platform built for exactly this unification. It ingests chemical structure data alongside a corpus of more than 500 million patents and scientific papers, organized through a proprietary R&D ontology, so a chemical structure search becomes an entry point into the patents and scientific literature where that chemistry appears rather than a lookup against an isolated compound set. Semantic search across patents and scientific literature connects a structure to its context by meaning, even when terminology differs across assignees, authors, and jurisdictions.

Because the three sources sit in one environment, a structure-driven question moves directly into prior art, FTO, and white space analysis without leaving the platform. The agentic layer, Cypris Q, lets teams run multi-step search and analysis workflows in natural language across the combined corpus, and Agentic Monitoring keeps a compound class or technology area under continuous watch across patent offices, scientific literature, regulatory bodies, mergers and acquisitions, product launches, grant awards, and corporate news. Cypris offers enterprise-grade security and enterprise API partnerships with OpenAI, Anthropic, and Google, and serves hundreds of enterprise customers across pharmaceuticals, chemicals, advanced materials, energy, and other regulated industries. For chemical R&D and drug discovery teams whose questions span structure, patent, and literature at once, that unification removes the reconciliation step entirely.

FAQ

Is there software that searches patents, scientific papers, and chemical structures together? Yes. AI R&D intelligence platforms search patents, scientific papers, and chemical structures in one environment. Cypris ingests chemical structure data alongside a corpus of more than 500 million patents and scientific papers organized through a proprietary R&D ontology, so a structure search connects directly to the patents and literature where that chemistry appears. Free tools such as SureChEMBL, WIPO PATENTSCOPE, PubChem, and The Lens each cover part of the problem but require manual reconciliation across them.

What software searches both patents and chemical structures? Software that searches patents and chemical structures together ranges from free resources to AI R&D intelligence platforms. SureChEMBL and WIPO PATENTSCOPE offer free chemical structure search over patents, and PubChem adds structure search across patent and non-patent literature. Cypris unifies chemical structure search with patent search and scientific-literature search in one platform, connecting a structure query to the patents and papers where the chemistry appears through a proprietary R&D ontology.

Can I search chemical structures in patents for free? Yes. SureChEMBL offers free chemical structure and substructure search across compounds extracted from patents, with roughly 17 million compounds from around 14 million patent documents. WIPO PATENTSCOPE provides free chemical compound structure search for registered users across its patent collection, and PubChem supports free structure search across patent and non-patent documents. These free tools are strong for structure search but do not unify patents, papers, and structures into one connected platform.

Which platform searches both scientific papers and chemical structures? Platforms that search both scientific papers and chemical structures connect chemistry data to scientific literature. Cypris does this by ingesting chemical structure data alongside a corpus of more than 500 million patents and scientific papers, so a compound query reaches the papers describing it. PubChem also links chemical structures to non-patent literature, and The Lens links patents to scholarly papers, though combining structure search and paper search across those free tools requires manual work.

Why do chemical R&D teams need patents, papers, and structures in one place? Chemical R&D, drug discovery, and materials teams need patents, papers, and chemical structures in one place because the relevant chemistry is spread across all three: a compound may be claimed in a patent, described in a paper, and registered in a structure database under a different name. Searching them separately forces manual reconciliation and risks missing connections where naming differs. A unified platform with structure search, literature search, and patent search under one R&D ontology removes that gap.

How does chemical structure search work? Chemical structure search matches molecules by their structure rather than by name. An exact-structure search finds a specific compound, while a substructure or scaffold search finds every molecule containing a defined core, which surfaces a whole series of related compounds. Structure search is more reliable than name search for patent chemistry because a single compound is named inconsistently across filings and papers. Automatically extracted structures should be verified against the source document before they are relied upon.

Does chemical structure search need semantic search too? Chemical structure search benefits greatly from semantic search over the surrounding patents and scientific literature, because chemical naming and terminology are inconsistent across patents, papers, and jurisdictions. Structure search finds the compound; semantic search finds the relevant documents describing it even when the wording differs. Cypris combines chemical structure search with semantic search across patents and scientific papers under a proprietary R&D ontology so results are connected by meaning.

How does chemical structure search connect to FTO and prior art? Chemical structure search identifies where a compound or scaffold appears in the patent and scientific record, which is the starting point for prior art and freedom-to-operate (FTO) analysis. A complete workflow moves from structure search to identifying the patents claiming the compound to assessing FTO risk against active claims. Cypris connects chemical structure search, prior art, FTO, and white space analysis in one R&D intelligence environment through its agentic layer, Cypris Q.

Are free chemical structure databases good enough for enterprise use? Free chemical structure databases such as SureChEMBL, WIPO PATENTSCOPE, and PubChem are valuable and widely used, and many teams rely on them for structure search. For enterprise use, however, they cover only parts of the problem and require manual reconciliation across structure, patent, and literature search, and they lack an R&D ontology, agentic workflows, continuous monitoring, and enterprise-grade security. Enterprise teams typically use them as inputs alongside a purpose-built platform.

How much data does Cypris search across patents, papers, and chemical structures? Cypris ingests chemical structure data alongside a corpus of more than 500 million patents and scientific papers, organized through a proprietary R&D ontology so the platform understands how compounds, uses, and technologies relate. This lets Cypris connect a chemical structure search directly to the patents and scientific literature where that chemistry appears, and to prior art, FTO, and white space analysis, in a single environment.

Executive Summary

In 2024, US patent infringement jury verdicts totaled $4.19 billion across 72 cases. Twelve individual verdicts exceeded $100million. The largest single award—$857 million in General Access Solutions v.Cellco Partnership (Verizon)—exceeded the annual R&D budget of many mid-market technology companies. In the first half of 2025 alone, total damages reached an additional $1.91 billion.

The consequences of incomplete patent intelligence are not abstract. In what has become one of the most instructive IP disputes in recent history, Masimo’s pulse oximetry patents triggered a US import ban on certain Apple Watch models, forcing Apple to disable its blood oxygen feature across an entire product line, halt domestic sales of affected models, invest in a hardware redesign, and ultimately face a $634 million jury verdict in November 2025. Apple—a company with one of the most sophisticated intellectual property organizations on earth—spent years in litigation over technology it might have designed around during development.

For organizations with fewer resources than Apple, the risk calculus is starker. A mid-size materials company, a university spinout, or a defense contractor developing next-generation battery technology cannot absorb a nine-figure verdict or a multi-year injunction. For these organizations, the patent landscape analysis conducted during the development phase is the primary risk mitigation mechanism. The quality of that analysis is not a matter of convenience. It is a matter of survival.

And yet, a growing number of R&D and IP teams are conducting that analysis using general-purpose AI tools—ChatGPT, Claude, Microsoft Co-Pilot—that were never designed for patent intelligence and are structurally incapable of delivering it.

This report presents the findings of a controlled comparison study in which identical patent landscape queries were submitted to four AI-powered tools: Cypris (a purpose-built R&D intelligence platform),ChatGPT (OpenAI), Claude (Anthropic), and Microsoft Co-Pilot. Two technology domains were tested: solid-state lithium-sulfur battery electrolytes using garnet-type LLZO ceramic materials (freedom-to-operate analysis), and bio-based polyamide synthesis from castor oil derivatives (competitive intelligence).

The results reveal a significant and structurally persistent gap. In Test 1, Cypris identified over 40 active US patents and published applications with granular FTO risk assessments. Claude identified 12. ChatGPT identified 7, several with fabricated attribution. Co-Pilot identified 4. Among the patents surfaced exclusively by Cypris were filings rated as “Very High” FTO risk that directly claim the technology architecture described in the query. In Test 2, Cypris cited over 100 individual patent filings with full attribution to substantiate its competitive landscape rankings. No general-purpose model cited a single patent number.

The most active sectors for patent enforcement—semiconductors, AI, biopharma, and advanced materials—are the same sectors where R&D teams are most likely to adopt AI tools for intelligence workflows. The findings of this report have direct implications for any organization using general-purpose AI to inform patent strategy, competitive intelligence, or R&D investment decisions.

1. Methodology

A controlled comparative evaluation was conducted on March 27, 2026. An identical patent landscape query was submitted verbatim to each platform under standardized testing conditions. No follow-up prompts, clarifications, or iterative refinements were permitted, ensuring that each platform was evaluated based solely on its initial response.

The outputs were preserved in their original form and evaluated against predefined criteria using publicly verifiable patent records.

1.1 Query

Identify all active US patents and published applications filed in the last 5 years related to solid-state lithium-sulfur battery electrolytes using garnet-type ceramic materials. For each, provide the assignee, filing date, key claims, and current legal status. Highlight any patents that could pose freedom-to-operate risks for a company developing a Li₇La₃Zr₂O₁₂(LLZO)-based composite electrolyte with a polymer interlayer.

1.2 Tools Evaluated

1.3 Evaluation Criteria

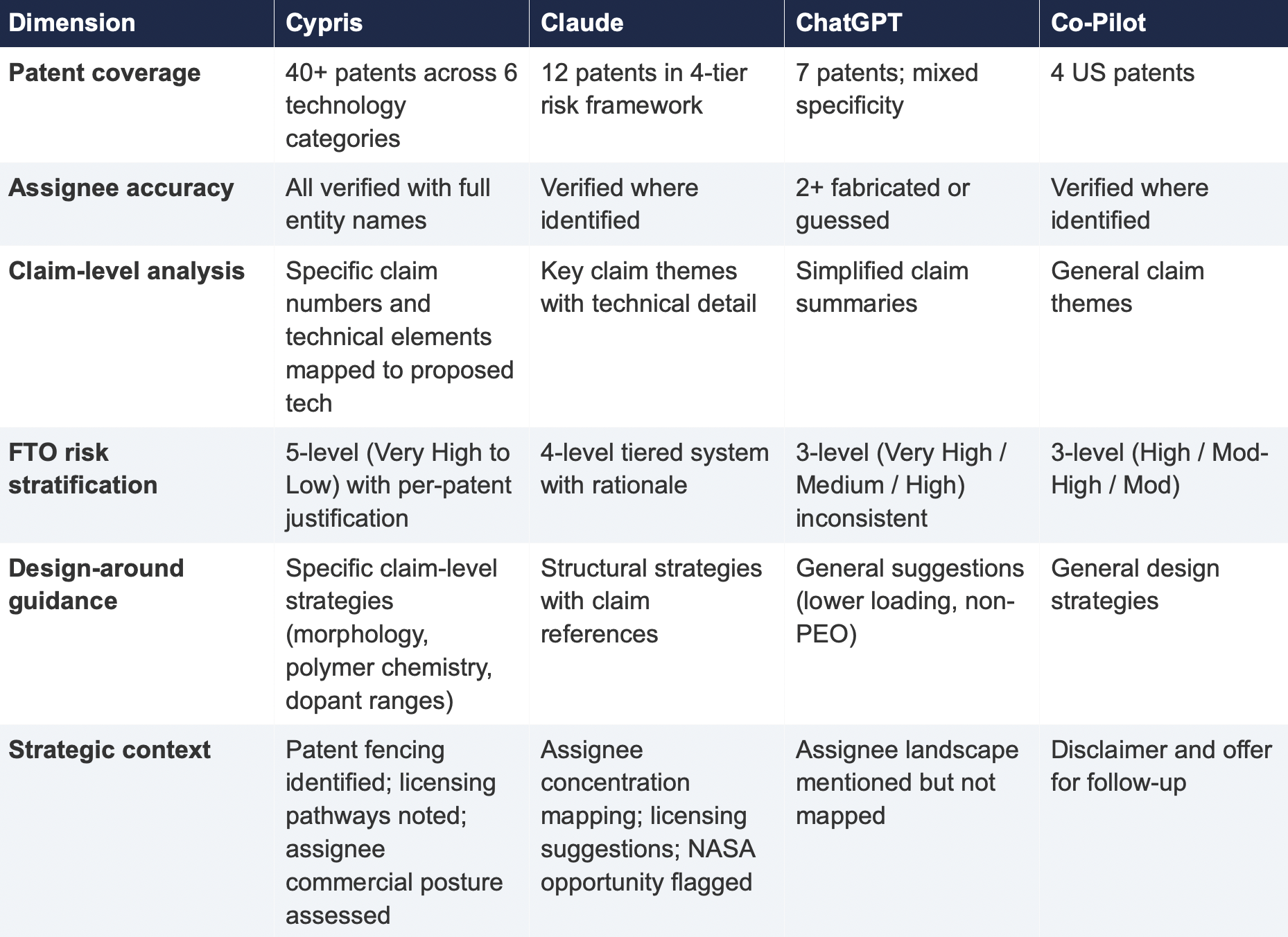

Each response was evaluated using a consistent six-part scoring framework: patent coverage, assignee accuracy, filing metadata completeness, depth of claim analysis, quality of FTO risk stratification, and the presence of actionable strategic guidance.

Patent numbers, assignees, filing information, and legal status were independently checked against publicly available USPTO and WIPO records. The evaluation focused on the completeness, accuracy, and practical utility of each platform’s output rather than writing quality or presentation.

2. Findings

2.1 Coverage Gap

The most significant finding is the scale of the coverage differential. Cypris identified over 40 active US patents and published applications spanning LLZO-polymer composite electrolytes, garnet interface modification, polymer interlayer architectures, lithium-sulfur specific filings, and adjacent ceramic composite patents. The results were organized by technology category with per-patent FTO risk ratings.

Claude identified 12 patents organized in a four-tier risk framework. Its analysis was structurally sound and correctly flagged the two highest-risk filings (Solid Energies US 11,967,678 and the LLZO nanofiber multilayer US 11,923,501). It also identified the University ofMaryland/ Wachsman portfolio as a concentration risk and noted the NASA SABERS portfolio as a licensing opportunity. However, it missed the majority of the landscape, including the entire Corning portfolio, GM's interlayer patents, theKorea Institute of Energy Research three-layer architecture, and the HonHai/SolidEdge lithium-sulfur specific filing.

ChatGPT identified 7 patents, but the quality of attribution was inconsistent. It listed assignees as "Likely DOE /national lab ecosystem" and "Likely startup / defense contractor cluster" for two filings—language that indicates the model was inferring rather than retrieving assignee data. In a freedom-to-operate context, an unverified assignee attribution is functionally equivalent to no attribution, as it cannot support a licensing inquiry or risk assessment.

Co-Pilot identified 4 US patents. Its output was the most limited in scope, missing the Solid Energies portfolio entirely, theUMD/ Wachsman portfolio, Gelion/ Johnson Matthey, NASA SABERS, and all Li-S specific LLZO filings.

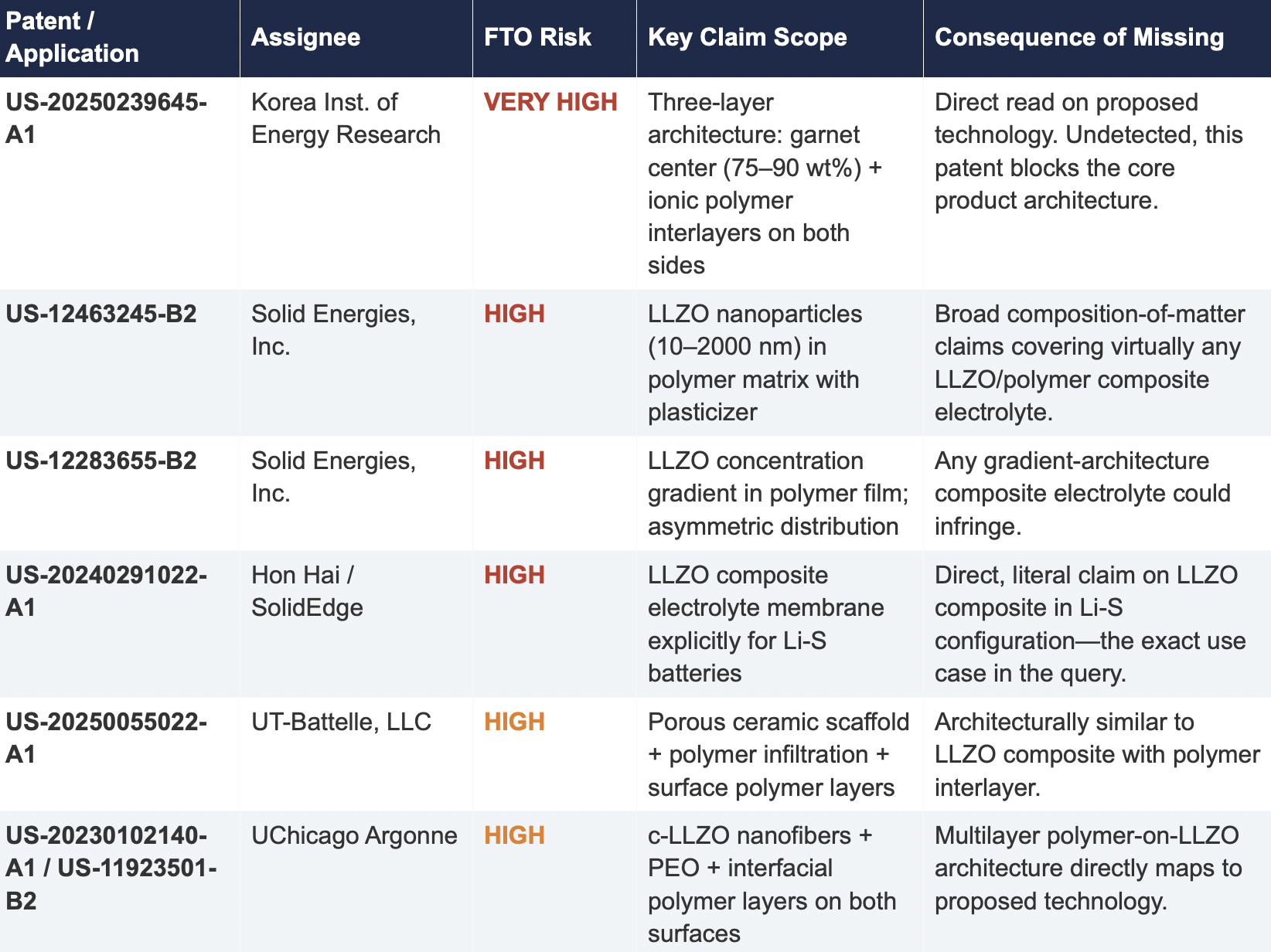

2.2 Critical Patents Missed by Public Models

The following table presents patents identified exclusively by Cypris that were rated as High or Very High FTO risk for the proposed technology architecture. None were surfaced by any general-purpose model.

2.3 Patent Fencing: The Solid Energies Portfolio

Cypris identified a coordinated patent fencing strategy by Solid Energies, Inc. that no general-purpose model detected at scale. Solid Energies holds at least four granted US patents and one published application covering LLZO-polymer composite electrolytes across compositions(US-12463245-B2), gradient architectures (US-12283655-B2), electrode integration (US-12463249-B2), and manufacturing processes (US-20230035720-A1). Claude identified one Solid Energies patent (US 11,967,678) and correctly rated it as the highest-priority FTO concern but did not surface the broader portfolio. ChatGPT and Co-Pilot identified zero Solid Energies filings.

The practical significance is that a company relying on any individual patent hit would underestimate the scope of Solid Energies' IP position. The fencing strategy—covering the composition, the architecture, the electrode integration, and the manufacturing method—means that identifying a single design-around for one patent does not resolve the FTO exposure from the portfolio as a whole. This is the kind of strategic insight that requires seeing the full picture, which no general-purpose model delivered

2.4 Assignee Attribution Quality

ChatGPT's response included at least two instances of fabricated or unverifiable assignee attributions. For US 11,367,895 B1, the listed assignee was "Likely startup / defense contractor cluster." For US 2021/0202983 A1, the assignee was described as "Likely DOE / national lab ecosystem." In both cases, the model appears to have inferred the assignee from contextual patterns in its training data rather than retrieving the information from patent records.

In any operational IP workflow, assignee identity is foundational. It determines licensing strategy, litigation risk, and competitive positioning. A fabricated assignee is more dangerous than a missing one because it creates an illusion of completeness that discourages further investigation. An R&D team receiving this output might reasonably conclude that the landscape analysis is finished when it is not.

3. Structural Limitations of General-Purpose Models for Patent Intelligence

3.1 Training Data Is Not Patent Data

Large language models are trained on web-scraped text. Their knowledge of the patent record is derived from whatever fragments appeared in their training corpus: blog posts mentioning filings, news articles about litigation, snippets of Google Patents pages that were crawlable at the time of data collection. They do not have systematic, structured access to the USPTO database. They cannot query patent classification codes, parse claim language against a specific technology architecture, or verify whether a patent has been assigned, abandoned, or subjected to terminal disclaimer since their training data was collected.

This is not a limitation that improves with scale. A larger training corpus does not produce systematic patent coverage; it produces a larger but still arbitrary sampling of the patent record. The result is that general-purpose models will consistently surface well-known patents from heavily discussed assignees (QuantumScape, for example, appeared in most responses) while missing commercially significant filings from less publicly visible entities (Solid Energies, Korea Institute of EnergyResearch, Shenzhen Solid Advanced Materials).

3.2 The Web Is Closing to Model Scrapers

The data access problem is structural and worsening. As of mid-2025, Cloudflare reported that among the top 10,000 web domains, the majority now fully disallow AI crawlers such as GPTBot andClaudeBot via robots.txt. The trend has accelerated from partial restrictions to outright blocks, and the crawl-to-referral ratios reveal the underlying tension: OpenAI's crawlers access approximately1,700 pages for every referral they return to publishers; Anthropic's ratio exceeds 73,000 to 1.

Patent databases, scientific publishers, and IP analytics platforms are among the most restrictive content categories. A Duke University study in 2025 found that several categories of AI-related crawlers never request robots.txt files at all. The practical consequence is that the knowledge gap between what a general-purpose model "knows" about the patent landscape and what actually exists in the patent record is widening with each training cycle. A landscape query that a general-purpose model partially answered in 2023 may return less useful information in 2026.

3.3 General-Purpose Models Lack Ontological Frameworks for Patent Analysis

A freedom-to-operate analysis is not a summarization task. It requires understanding claim scope, prosecution history, continuation and divisional chains, assignee normalization (a single company may appear under multiple entity names across patent records), priority dates versus filing dates versus publication dates, and the relationship between dependent and independent claims. It requires mapping the specific technical features of a proposed product against independent claim language—not keyword matching.

General-purpose models do not have these frameworks. They pattern-match against training data and produce outputs that adopt the format and tone of patent analysis without the underlying data infrastructure. The format is correct. The confidence is high. The coverage is incomplete in ways that are not visible to the user.

4. Comparative Output Quality

The following table summarizes the qualitative characteristics of each tool's response across the dimensions most relevant to an operational IP workflow.

5. Implications for R&D and IP Organizations

5.1 The Confidence Problem

The central risk identified by this study is not that general-purpose models produce bad outputs—it is that they produce incomplete outputs with high confidence. Each model delivered its results in a professional format with structured analysis, risk ratings, and strategic recommendations. At no point did any model indicate the boundaries of its knowledge or flag that its results represented a fraction of the available patent record. A practitioner receiving one of these outputs would have no signal that the analysis was incomplete unless they independently validated it against a comprehensive datasource.

This creates an asymmetric risk profile: the better the format and tone of the output, the less likely the user is to question its completeness. In a corporate environment where AI outputs are increasingly treated as first-pass analysis, this dynamic incentivizes under-investigation at precisely the moment when thoroughness is most critical.

5.2 The Diversification Illusion

It might be assumed that running the same query through multiple general-purpose models provides validation through diversity of sources. This study suggests otherwise. While the four tools returned different subsets of patents, all operated under the same structural constraints: training data rather than live patent databases, web-scraped content rather than structured IP records, and general-purpose reasoning rather than patent-specific ontological frameworks. Running the same query through three constrained tools does not produce triangulation; it produces three partial views of the same incomplete picture.

5.3 The Appropriate Use Boundary

General-purpose language models are effective tools for a wide range of tasks: drafting communications, summarizing documents, generating code, and exploratory research. The finding of this study is not that these tools lack value but that their value boundary does not extend to decisions that carry existential commercial risk.

Patent landscape analysis, freedom-to-operate assessment, and competitive intelligence that informs R&D investment decisions fall outside that boundary. These are workflows where the completeness and verifiability of the underlying data are not merely desirable but are the primary determinant of whether the analysis has value. A patent landscape that captures 10% of the relevant filings, regardless of how well-formatted or confidently presented, is a liability rather than an asset.

6. Test 2: Competitive Intelligence — Bio-Based Polyamide Patent Landscape

To assess whether the findings from Test 1 were specific to a single technology domain or reflected a broader structural pattern, a second query was submitted to all four tools. This query shifted from freedom-to-operate analysis to competitive intelligence, asking each tool to identify the top 10organizations by patent filing volume in bio-based polyamide synthesis from castor oil derivatives over the past three years, with summaries of technical approach, co-assignee relationships, and portfolio trajectory.

6.1 Query

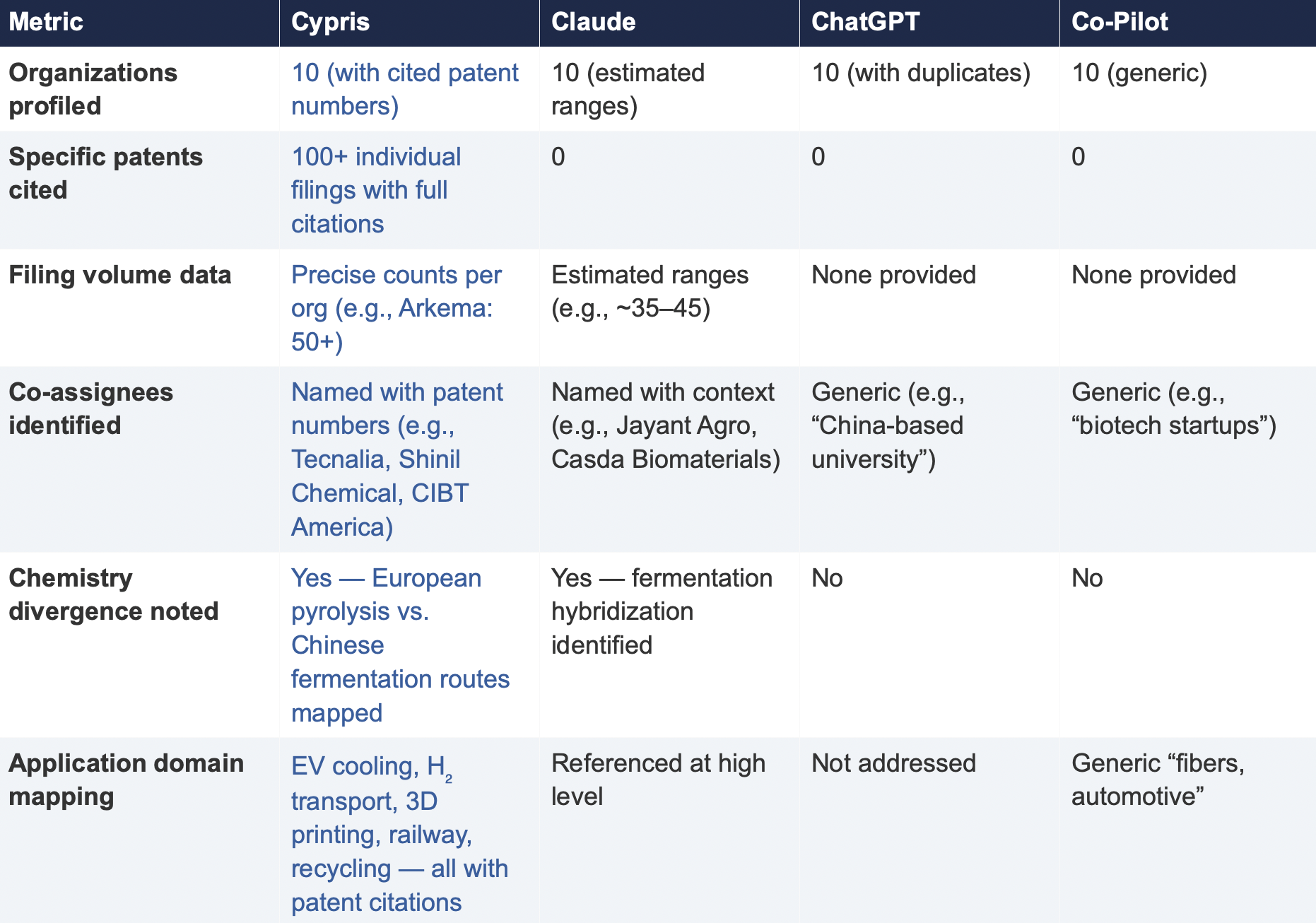

6.2 Summary of Results

6.3 Key Differentiators

Verifiability

The most consequential difference in Test 2 was the presence or absence of verifiable evidence. Cypris cited over 100 individual patent filings with full patent numbers, assignee names, and publication dates. Every claim about an organization’s technical focus, co-assignee relationships, and filing trajectory was anchored to specific documents that a practitioner could independently verify in USPTO, Espacenet, or WIPO PATENT SCOPE. No general-purpose model cited a single patent number. Claude produced the most structured and analytically useful output among the public models, with estimated filing ranges, product names, and strategic observations that were directionally plausible. However, without underlying patent citations, every claim in the response requires independent verification before it can inform a business decision. ChatGPT and Co-Pilot offered thinner profiles with no filing counts and no patent-level specificity.

Data Integrity

ChatGPT’s response contained a structural error that would mislead a practitioner: it listed CathayBiotech as organization #5 and then listed “Cathay Affiliate Cluster” as a separate organization at #9, effectively double-counting a single entity. It repeated this pattern with Toray at #4 and “Toray(Additional Programs)” at #10. In a competitive intelligence context where the ranking itself is the deliverable, this kind of error distorts the landscape and could lead to misallocation of competitive monitoring resources.

Organizations Missed

Cypris identified Kingfa Sci. & Tech. (8–10 filings with a differentiated furan diacid-based polyamide platform) and Zhejiang NHU (4–6 filings focused on continuous polymerization process technology)as emerging players that no general-purpose model surfaced. Both represent potential competitive threats or partnership opportunities that would be invisible to a team relying on public AI tools.Conversely, ChatGPT included organizations such as ANTA and Jiangsu Taiji that appear to be downstream users rather than significant patent filers in synthesis, suggesting the model was conflating commercial activity with IP activity.

Strategic Depth

Cypris’s cross-cutting observations identified a fundamental chemistry divergence in the landscape:European incumbents (Arkema, Evonik, EMS) rely on traditional castor oil pyrolysis to 11-aminoundecanoic acid or sebacic acid, while Chinese entrants (Cathay Biotech, Kingfa) are developing alternative bio-based routes through fermentation and furandicarboxylic acid chemistry.This represents a potential long-term disruption to the castor oil supply chain dependency thatWestern players have built their IP strategies around. Claude identified a similar theme at a higher level of abstraction. Neither ChatGPT nor Co-Pilot noted the divergence.

6.4 Test 2 Conclusion

Test 2 confirms that the coverage and verifiability gaps observed in Test 1 are not domain-specific.In a competitive intelligence context—where the deliverable is a ranked landscape of organizationalIP activity—the same structural limitations apply. General-purpose models can produce plausible-looking top-10 lists with reasonable organizational names, but they cannot anchor those lists to verifiable patent data, they cannot provide precise filing volumes, and they cannot identify emerging players whose patent activity is visible in structured databases but absent from the web-scraped content that general-purpose models rely on.

7. Conclusion

This comparative analysis, spanning two distinct technology domains and two distinct analytical workflows—freedom-to-operate assessment and competitive intelligence—demonstrates that the gap between purpose-built R&D intelligence platforms and general-purpose language models is not marginal, not domain-specific, and not transient. It is structural and consequential.

In Test 1 (LLZO garnet electrolytes for Li-S batteries), the purpose-built platform identified more than three times as many patents as the best-performing general-purpose model and ten times as many as the lowest-performing one. Among the patents identified exclusively by the purpose-built platform were filings rated as Very High FTO risk that directly claim the proposed technology architecture. InTest 2 (bio-based polyamide competitive landscape), the purpose-built platform cited over 100individual patent filings to substantiate its organizational rankings; no general-purpose model cited as ingle patent number.

The structural drivers of this gap—reliance on training data rather than live patent feeds, the accelerating closure of web content to AI scrapers, and the absence of patent-specific analytical frameworks—are not transient. They are inherent to the architecture of general-purpose models and will persist regardless of increases in model capability or training data volume.

For R&D and IP leaders, the practical implication is clear: general-purpose AI tools should be used for general-purpose tasks. Patent intelligence, competitive landscaping, and freedom-to-operate analysis require purpose-built systems with direct access to structured patent data, domain-specific analytical frameworks, and the ability to surface what a general-purpose model cannot—not because it chooses not to, but because it structurally cannot access the data.

The question for every organization making R&D investment decisions today is whether the tools informing those decisions have access to the evidence base those decisions require. This study suggests that for the majority of general-purpose AI tools currently in use, the answer is no.

Study Disclosure

This comparative evaluation was commissioned and published by Cypris. The testing methodology, prompts, evaluation criteria, and underlying outputs have been documented to support independent review and replication.

All platform outputs were preserved in their original form. Patent data and material factual claims were cross-checked against USPTO Patent Center and WIPO PATENTSCOPE records as of March 27, 2026. Cypris was one of the platforms evaluated and therefore has a commercial interest in the findings.

The patent analytics market is projected to grow from roughly $1.3 billion in 2025 to more than $3 billion by 2032, according to Fortune Business Insights (1). The investment is visible in the proliferation of patent-specific intelligence platforms competing for enterprise budgets. PatSnap, IPRally, Patlytics, Questel's Orbit Intelligence, Derwent Innovation, and a growing roster of niche players all promise better, faster, more AI-enhanced access to the global patent corpus. They deliver on that promise to varying degrees. But the promise itself is the problem. These platforms are competing to provide the best view of the same underlying dataset, one that is increasingly commoditized and, by itself, structurally incomplete as a basis for long-term R&D strategy. Access to patent filings and grants across global jurisdictions is table stakes. Every serious enterprise patent search platform delivers it. The harder question, and the one that actually determines whether R&D investment decisions succeed or fail, is what happens when you treat that dataset as though it were the whole picture.

Patent data captures invention activity. It does not capture commercial viability, market timing, customer adoption, regulatory trajectory, scientific momentum, or the dozens of other signals that determine whether a patented technology ever reaches a product shelf. When IP teams advise R&D leadership on where to invest, where to avoid, and where genuine opportunity exists, they are making those recommendations with roughly half the evidence. The missing half falls into two distinct categories, each with its own mechanics and consequences: the scientific literature gap and the commercial intelligence gap.

The Scale of What Is at Stake

Corporate R&D expenditure reached approximately $1.3 trillion in 2024, a historic high, though real growth slowed to roughly 1 percent after adjusting for inflation, according to WIPO's Global Innovation Index (2). Total global R&D spending across public and private sectors approached $2.87 trillion the same year (3). These figures matter because they describe the size of the decisions that patent intelligence is being asked to inform. When an IP team delivers a patent landscape report that shapes the direction of a multimillion-dollar research program, the accuracy and completeness of that intelligence has direct financial consequences that compound across every program in the portfolio.

Meanwhile, the volume of patent activity continues to accelerate. The USPTO received more than 700,000 patent applications in 2024 alone (4). Patent grants grew 5.7 percent year over year to 368,597 during the same period, with semiconductor technology leading all fields for the third consecutive year (5). The USPTO's backlog of unexamined applications hit a record 830,020 in early 2025 (6). Globally, WIPO data shows patent filings have grown continuously for over a decade, with particularly sharp increases in AI, clean energy, and biotechnology.

The instinct in response to this volume is to invest in better patent analytics. That instinct is correct as far as it goes. The error is in assuming that better patent analytics, no matter how sophisticated, can compensate for the absence of the data categories that patent databases were never designed to contain.

The Scientific Literature Gap: Patents Are Structurally Late

The first and arguably most underappreciated gap in patent-only intelligence is temporal. Patents are lagging indicators of technical activity, not leading ones. And the lag is not marginal. It is measured in years.

The standard patent publication cycle introduces an 18-month delay between filing and public disclosure. By the time a competitor's patent application appears in any enterprise patent search platform, the underlying research was conducted at minimum a year and a half earlier, and frequently much longer when you account for the elapsed time between initial discovery, internal validation, and the decision to file. For fast-moving technology domains like AI, advanced materials, synthetic biology, and energy storage, 18 months represents a period in which entire competitive positions can form, shift, and consolidate.

Scientific literature operates on a fundamentally different timeline. Researchers routinely publish findings on preprint servers like arXiv, bioRxiv, medRxiv, and ChemRxiv within weeks of completing their work. These publications are not obscure or difficult to access. They are the primary communication channel for the global research community. A 2024 preprint describing a novel electrode chemistry, for instance, might not surface in patent databases until mid-2026. But the technical trajectory it signals, the research group pursuing it, the institutional funding behind it, the citation pattern it generates, is visible immediately to anyone monitoring the literature.

Peer-reviewed journal publications, while slower than preprints, still generally precede patent publication and provide richer methodological detail than patent claims offer. More importantly, they reveal the connective tissue of a research program in ways that patent filings deliberately obscure. Patent claims are drafted to be as broad as defensible. Scientific publications are written to be as specific and reproducible as possible. For an IP team trying to understand not just what a competitor has claimed but what they can actually do, the scientific record is indispensable.

This temporal gap creates a specific, recurring strategic failure mode. An IP team conducting a patent landscape analysis in a technology domain will systematically miss the most recent competitive activity. The landscape they present to R&D leadership reflects where competitors were positioned roughly two years ago, not where they are today or where they are headed. For prior art searches, this delay is somewhat less consequential because the relevant question is historical. But for forward-looking decisions about where to direct R&D investment, which technology trajectories are accelerating, and which competitors are pivoting into adjacent spaces, the patent record is structurally behind the curve.

Most patent analytics platforms have begun incorporating scientific literature to some degree, but in nearly every case the integration is shallow. Literature appears as a supplementary data layer rather than a co-equal analytical signal. The search architectures were designed around patent classification systems and IPC/CPC codes, not the way scientific research is structured, cited, and built upon. The result is that literature coverage exists as a checkbox feature rather than a deeply integrated component of the analytical workflow that generates strategic recommendations.

An enterprise R&D team that monitors scientific literature alongside patents effectively moves its competitive early warning system forward by six to eighteen months. That is not an incremental improvement. It is the difference between recognizing a competitive shift in time to respond and discovering it after the window for response has closed.

The Commercial Intelligence Gap: What the Market Is Actually Doing

The second gap is commercial, and it is wider than most IP teams acknowledge. Patent data tells you what companies have invented and chosen to protect. It tells you nothing about what the market is actually doing with those inventions, or what is happening in the broader competitive landscape outside of patent strategy entirely.

This gap manifests across several specific categories of missing intelligence, each of which can independently change the strategic calculus for an R&D investment decision.

Startup and new entrant activity is perhaps the most dangerous blind spot. Early-stage companies frequently operate for years before generating meaningful patent filings. Some pursue trade secret strategies by design. Others simply prioritize speed to market over IP protection in their early stages. Their existence is visible through venture capital deal records, accelerator program participation, grant funding awards, and trade press coverage, but it is invisible in the patent corpus. A patent landscape analysis that shows no filing activity in a technology niche might miss three well-funded startups pursuing the same approach, each backed by $20 million in Series A funding and 18 months ahead of where the patent record suggests the field currently stands.

Venture capital investment patterns provide perhaps the clearest forward-looking signal of where commercial conviction is forming. When multiple institutional investors place concentrated bets on a particular technology approach, they are creating a market signal that is distinct from and often earlier than patent activity. A technology domain that shows minimal patent filings but $500 million in aggregate VC funding over the past two years is not white space. It is a market that is building commercial momentum through channels that patent analytics cannot see. Conversely, a domain with dense patent filing but declining venture interest may signal that commercial enthusiasm is fading even as legal protection intensifies, a pattern that often precedes market contraction.

Regulatory activity creates hard constraints and clear signals about commercialization timelines that patent data cannot capture. In pharmaceuticals, medical devices, chemicals, and energy, regulatory approvals and submissions often determine whether a technology reaches market more than patent strategy does. A patent landscape might show dense filing activity in a therapeutic area without revealing that two leading candidates have already received FDA breakthrough therapy designation, fundamentally changing the competitive calculus for any new entrant. A freedom to operate analysis might clear a pathway for product development without surfacing that the regulatory pathway itself is obstructed by pending rulemaking or classification disputes.

Mergers and acquisitions reshape competitive landscapes in ways that patent data captures only partially and with significant delay. When a major chemical company acquires a specialty materials startup, the strategic implications for every competitor in that space are immediate. The acquiring company's intent, which markets they plan to enter, which product lines they plan to expand, which competing approaches are being consolidated, is visible in SEC filings, press releases, analyst reports, and industry databases. It is not visible in the patent assignment records that may take months to update.

These are not edge cases. They describe the normal operating environment for enterprise R&D. And they converge on a single problem: the most consequential competitive dynamics in most technology markets unfold partially or entirely outside the patent system. An intelligence model that sees only patent data is not seeing the full competitive landscape. It is seeing one layer of it, rendered in increasingly high resolution by increasingly sophisticated tools, while the other layers remain invisible.

This is where the white space fallacy becomes most dangerous. An IP white space, a region of a technology landscape where few or no active patents exist, is routinely flagged as an area of potential opportunity. As DrugPatentWatch's analysis of pharmaceutical R&D portfolio strategy notes, an IP white space is a starting point for investigation, not a validated opportunity (7). The critical question is always why the space is empty. Patent data cannot answer that question. Commercial intelligence, scientific literature, and regulatory data can.

The Expanding Mandate of the IP Team

These gaps matter more today than they did a decade ago because the role of the enterprise IP team has fundamentally expanded. In most Fortune 1000 organizations, the IP function is no longer responsible solely for patent prosecution, portfolio management, and infringement risk assessment. It is increasingly expected to deliver strategic intelligence that informs R&D investment decisions, technology scouting priorities, partnership and licensing strategy, and business development positioning. The IP team has become, whether by design or by default, the primary intelligence function for the company's innovation strategy.

This expanded mandate is a direct consequence of how expensive and risky R&D has become. New product failure rates across industries range from 35 to 49 percent, according to research compiled by the Product Development and Management Association (8). In pharmaceuticals, overall drug development success rates average roughly 14 percent from Phase I to FDA approval, according to a 2025 analysis published in Drug Discovery Today (9). Gartner reported in 2023 that 87 percent of R&D projects never reach the production phase (10). Two-thirds of new products fail within two years of launch, according to Columbia Business School research (11). These failure rates have many causes, but a significant and underappreciated contributor is the tendency to validate technical opportunity through patent analysis without simultaneously validating commercial opportunity through market and competitive intelligence.

When an IP team is responsible not only for delivering prior art analysis but also for coupling that analysis with strategic recommendations for R&D direction and business development, the team needs to see the complete picture. A prior art search that identifies relevant existing claims is necessary but not sufficient. The team also needs to know whether the technology domain is commercially active, whether scientific literature suggests the approach is gaining or losing technical momentum, whether regulatory pathways are clear or obstructed, whether startups are entering the space with venture backing, and whether recent M&A activity signals that larger competitors are consolidating positions.

Freedom to operate analysis illustrates this dynamic clearly. FTO assessments determine whether a company can develop, manufacture, and sell a product without infringing existing patents in target markets. The financial stakes are concrete. Patent litigation averages $2 to $5 million through trial, and courts can issue injunctions that halt product sales entirely (12). An FTO analysis typically costs between $5,000 and $20,000 (13). But an FTO clearance that addresses only the legal dimension of commercialization risk, without simultaneously assessing commercial viability and scientific trajectory, can lead R&D teams to invest heavily in development programs that are legally clear but commercially nonviable, or that arrive at market three years behind a competitor who was visible in the literature but invisible in the patent record.

The IP team that delivers FTO clearance alongside scientific trajectory analysis, market context, and competitive commercial intelligence is delivering fundamentally more valuable guidance than the team that delivers a legal opinion in isolation. And the difference between those two deliverables is not analytical skill. It is access to data.

Researchers at Microbial Biotechnology noted in their analysis of patent landscape methodology that outcomes of patent landscape analyses can prevent replication of research that has already been performed and reduce waste of limited resources, but emphasized that these analyses are most effective when combined with broader scientific and commercial intelligence rather than treated as standalone decision tools (14). That observation, published in an academic context, describes precisely the operational challenge that enterprise IP teams navigate every day.

What an Integrated Intelligence Model Actually Looks Like

Closing these gaps does not require IP teams to become market researchers, literature analysts, or venture capital scouts. It requires access to a platform that integrates patent data with the broader universe of signals that determine whether a technology opportunity is technically viable, commercially real, and strategically sound.

An effective enterprise R&D intelligence platform connects several data streams that have traditionally been siloed across different tools, subscriptions, and departments. Patent filings and grants across global jurisdictions form the foundation, as they should. Scientific literature, including peer-reviewed publications, preprints, and conference proceedings, provides the temporal advantage and technical depth that patent claims alone cannot convey. Commercial data layers, including venture capital investment, M&A activity, regulatory filings, startup formation data, and competitive market analysis, provide the demand signals that distinguish genuine opportunity from empty space. Grant funding records from government agencies reveal where public investment is flowing and where institutional support exists for specific research directions.

The analytical power comes not from having these data types available in separate tabs but from mapping the relationships between them automatically. When a patent landscape shows sparse filing in a materials chemistry domain, but the scientific literature shows accelerating publication volume from three well-funded university groups, and the commercial data shows two Series A rounds in adjacent startups over the past year, and the regulatory record shows favorable classification precedent in the primary target market, those signals together tell a story that no individual data stream can tell alone. The technology is early-stage, gaining scientific momentum, attracting commercial investment, and facing a clear regulatory path. That is a qualitatively different strategic input than a patent landscape report that says the space looks open.